Businesses that haven’t optimized their payment operations don’t understand what it’s truly costing them—and it’s a lot more than they might think.

In 2020, failed payments and poor payment operations cost the global economy $118.5 billion. On top of that, Accounts Payable personnel spend 30% of their time answering questions and tracking down information or documents, two tasks that represent only part of the burden of manual payment processes. By handling transactions the old-fashioned way in the age of digital innovation, companies waste a significant amount of time—and time, as we know, is money.

75% of businesses are holding onto these legacy payment systems, using paper checks in lieu of modern digital solutions. And while the idea of digitally transforming payment operations may seem daunting—especially for older companies or businesses with a large backlog of paper to sort through—it’s crucial for businesses to modernize their systems to remain competitive and efficient.

In this blog, we’ll share the problems you may not know are impacting your business and how the right payments automation solution can help.

#1 Slow Processing: The Cash Flow Killer

Manual payments – paper checks, manual data entry and file-based processes – are inherently slower than automated systems. This can delay initiating, approving and completing payment transactions.

- Slowdowns in accounts receivable can lead to inadequate cash flow and working capital constraints.

- Slow processing of accounts payable can strain vendor relationships and eventually create supply chain issues.

- Any payment processing slowdown is detrimental to customer experience.

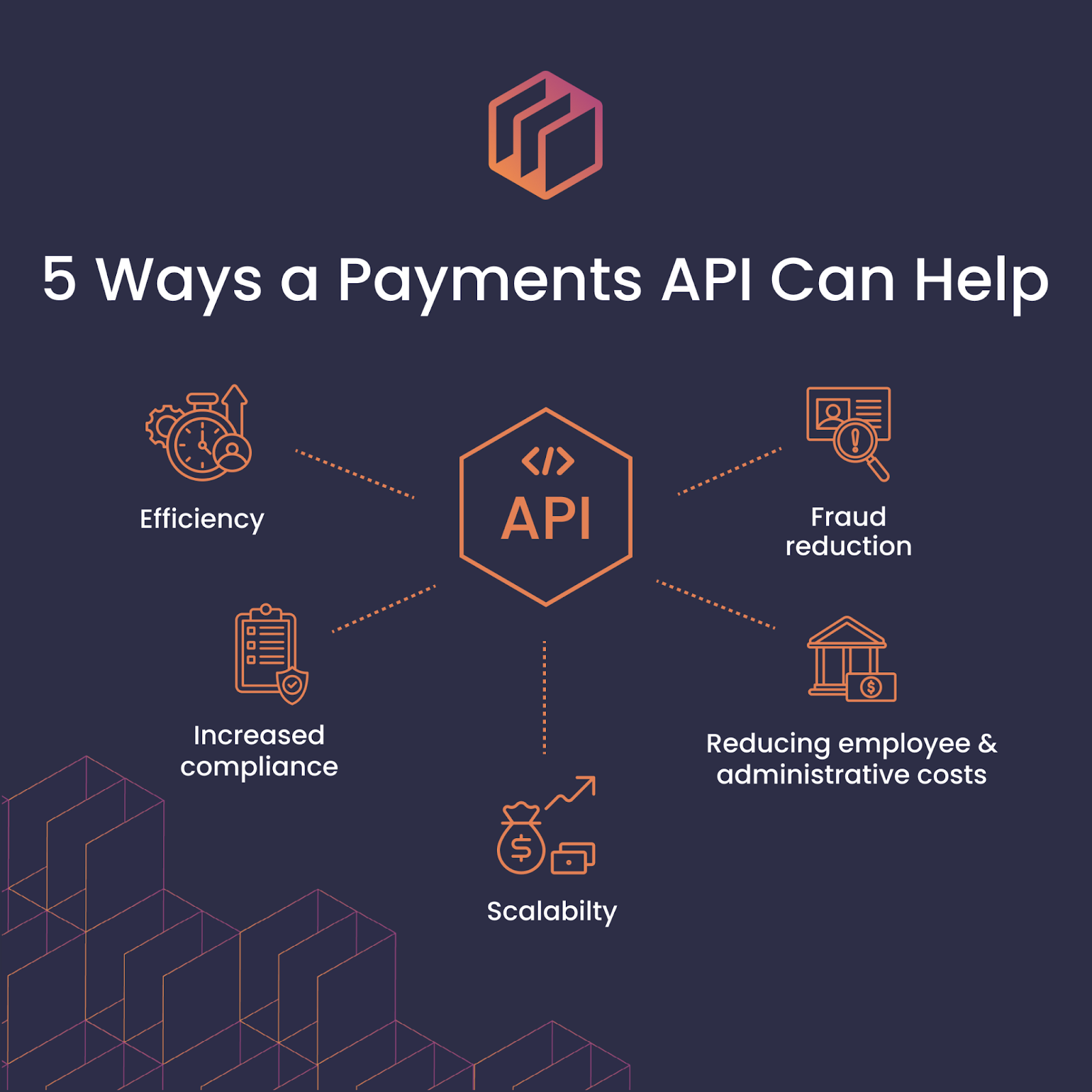

- Switching to automated payments can dramatically improve cash flow.

#2 Errors: The Cost of Human Fallibility

Human errors are inevitable and contribute significantly to a slow payment cycle and increased costs. The more manual steps involved in a transaction, the greater the chance of mistakes.

- Data entry and matching can be tedious and time-consuming, leading to longer processing times, higher labor costs, and, of course, more errors.

- Manual payment processing typically has a higher margin of error, and correcting those errors requires exception-handling processes and approvals. All of these rework steps take time, and at scale, this time translates to significant financial losses.

- ACH payment automation minimizes these errors.

#3 Failed Payments: The Ripple Effect

Payment failures occur for various reasons: expired credit cards, incorrect payment details, insufficient funds or fraud detection.

- Failed payments require time and effort to identify the problem, resolve it and reprocess the payment.

- Manual payment processes exacerbate the impact of these issues, especially if multiple platforms are involved and they don’t communicate effectively. Invoicing, approvals and payment initiation might be siloed, making it difficult to catch issues early.

- Automated payment systems can provide better communication, access to data and payment tracking and flags for failures.

#4 Direct and Indirect Costs: The Hidden Expenses

Processing payments manually incurs both direct and indirect expenses. Direct expenses include supplies (paper, envelopes, ink and postage), and wages for employees who spend time printing invoices, preparing checks and mailing payments.

- Manually matching invoice numbers, issuing purchase orders after invoice approval and collecting signatures can be tedious and time-consuming.

Indirect costs are equally significant. The time spent on manual payments could be used for more strategic activities, like increasing efficiency and productivity.

- Companies using manual payments may miss out on business opportunities and strategic partnerships because they know their current manual processes can’t handle increased volumes.

#5 Inadequate Payment Security: The Risk of Fraud

The vulnerability to fraud is higher with manual payments. Manual data entry and paper-based systems create more opportunities to tamper with payments, and the limited audit trail makes it harder to trace fraudulent activity.

- Without real-time monitoring and automated fraud detection mechanisms, businesses are more exposed to fraudulent activities that may go undetected for extended periods.

- This lack of timely intervention can lead to substantial losses and compromise the security of payment systems.

- Secure ACH transfers and automated systems significantly mitigate these risks.

The Solution? Embrace Automation

The solution lies in embracing payment automation. Modern payment solutions, like Dwolla's API, help streamline the payment process, eliminating the inefficiencies and risks associated with manual payment methods.

By automating ACH payments and enabling real-time payment processing, businesses can significantly reduce costs associated with paper handling and manual errors. Automated solutions help enhance security through features like tokenization and encryption, mitigating the vulnerabilities of traditional payment methods.

Investing in payment automation with a platform like Dwolla isn't just about improving current operations; it's a strategic investment in the future of your business and can position you for growth, efficiency and a competitive edge. Schedule a payments consultation with our team today!