2025 Guide: Understanding A2A Payments and Their Role in Insurance Payment Processing

In this guide, we will cover:

- Digital Transformation in Insurance: Why Now?

- Common Challenges and Solutions in Insurance Payment Processing

- Benefits of Using A2A Payments for Insurance Payments

- How A2A Payments Can Save an Insurance Company Money

- How A2A Payments Improve Efficiency by Streamlining Insurance Payment Processing

- Security Measures in A2A Payments for Insurance Transactions

- Regulatory Compliance Considerations for A2A Payments in Insurance

- Integrating A2A Payments into Your Insurance Payment Operations

- Future Trends and Innovations in A2A Insurance Payment Processing

Account-to-account (A2A) payments (also known as pay by bank payments)—including ACH, RTP and FedNow transfers—play a crucial role in streamlining insurance payment processing. These modern payment solutions offer benefits such as efficiency, speed and security to reduce payment processing costs and improve customer satisfaction.

Here’s a little background on the types of A2A payments:

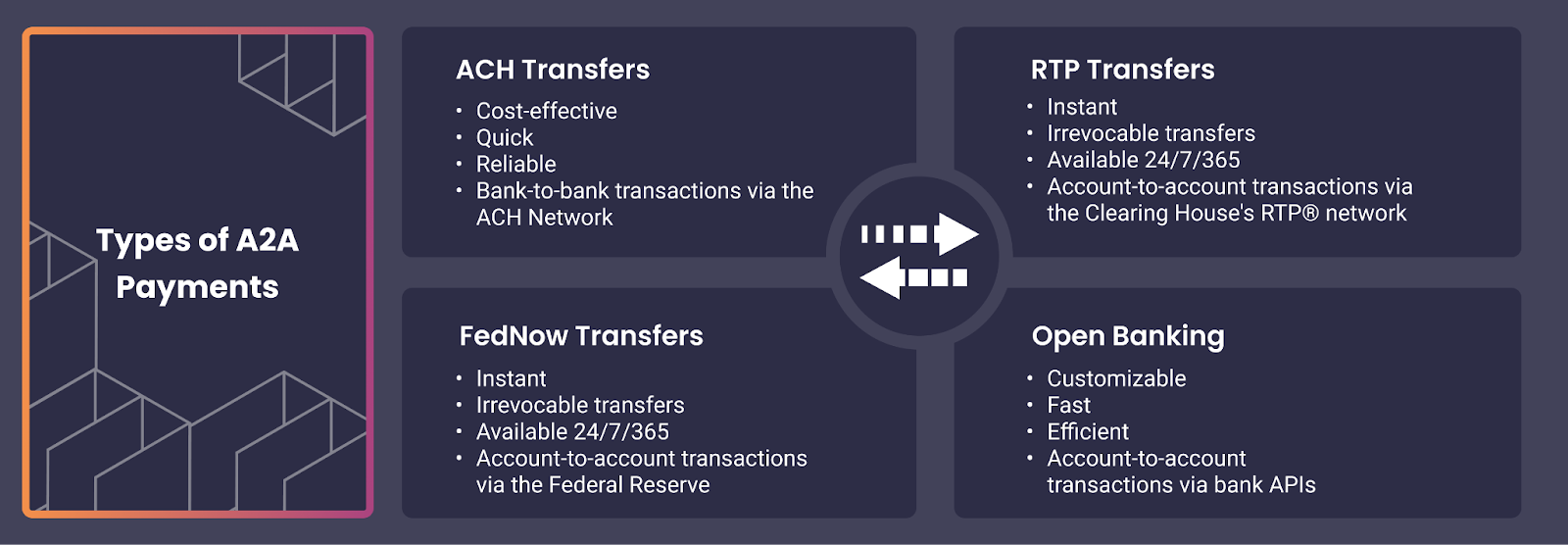

ACH Transfers

Cost-effective and reliable, Automated Clearing House (ACH) payments are widely used in the insurance industry. These bank-to-bank transfers are processed reliably via the ACH Network, operated by the National Automated Clearing House Association (Nacha). After a typical ACH transaction is initiated, funds are available in the recipient’s bank account in 1-5 business days. For those who need faster speeds, Same Day ACH allows a credit to or debit from a bank account to settle within the same business day. These solutions starkly contrast with traditional manual payment methods, like paper checks and credit card payments, which take longer to process and can have increased instances of human error, theft, and fraud.

RTP Transfers

Real-Time Payments (RTP) are account-to-account transactions that are sent via The Clearing House’s RTP® network which clear and settle nearly instantaneously 24/7/365. RTP transactions are mostly credit-only transfers, meaning they can be used to send funds, but not debit or pull funds from someone else’s account. RTP transactions also support extensive remittance data that can be used to reconcile funds efficiently, and since the transactions settle within seconds, all transfers are irrevocable. Alternatively, demand certainly exists for real-time debits, known as Request for Payment (RFP), and instant payments organizations continue to explore how they can provide instant payment functionality for RFP use cases.

FedNow Transfers

The FedNow® Service is an instant payment system created by the Federal Reserve that enables banks and credit unions to offer their customers the ability to send and receive payments in near real-time, 24 hours a day, seven days a week, 365 days a year. It is similar to the RTP network in that the payments are mostly credit-only transfers while participants work to determine the best way to provide payments for RFP use cases. FedNow also provides extensive remittance data and irrevocable transfers.

Open Banking

A2A payments are made possible with open banking, which uses application programming interfaces (APIs) to enable the secure exchange of consumer data and financial information between different financial institutions and authorized third-party providers (TPPs). In the payments space, open banking tools can be used to verify bank accounts information, such as ownership and account balances, prior to initiating a transaction. These verification steps and checks can help streamline the onboarding process and help mitigate and reduce fraud and returned payments.

Dwolla modernizes insurance payment processing by streamlining A2A payments and automation, replacing outdated payment methods with cost-effective, flexible, secure, and fast payment solutions. In this guide, we’ll explore the wide range of applications for A2A payments in insurance, highlighting benefits, outlining challenges, and sharing advice on successfully integrating A2A payment solutions for your business needs.

Digital Transformation in Insurance: Why Now?

Policyholders crave digital convenience and faster reimbursements. The companies that meet this demand are gaining a competitive edge.

The proof is in the data:

- More than one-quarter of policyholders switch providers to achieve faster payouts.

- 65% of millennials and Gen Z policyholders expect instant payment options through mobile apps.

- The global digital payments market is projected to reach a staggering $60.8 trillion by 2027, a 47% increase from 2023.

Digital transformation in insurance payments isn't optional – it's akin to survival. Major pain points that plague the insurance industry, sparking a need for immediate change include:

- Legacy payment methods and manual processes slow down insurance payments, increase the likelihood of human error, and cost significant time and money.

- Slow claim payments and poor payment experiences lead to policyholder attrition.

Businesses stuck in legacy payment systems risk not only falling behind but missing out on critical market share and competitive advantages.

Common Challenges and Solutions in Insurance Payment Processing

The insurance industry is facing a digital revolution, and payments processing is at the forefront of this change. Legacy systems are slowing down operations, leaving data vulnerable, and failing to meet the expectations of today's policyholders.

Digital Transformation

One of the biggest challenges for insurers is adopting digital transformation in payment processing. Insurers must consider the costs of replacing outdated technologies, tools, and systems in addition to the amount of time required to securely and efficiently upgrade.

While change can’t happen overnight, digital transformation in payments is becoming necessary. Legacy systems slow down payment cycles and internal operations while threatening the security of policyholder data. Fraud in payments is growing and advancing alongside technology, so outdated payment processing systems create vulnerabilities and leave insurance companies behind.

As policyholders overwhelmingly favor digital transactions, insurers must adapt their claims management software to remain competitive and provide a positive, more secure policyholder experience. This may require investing in new technologies and tools, but the long-term benefits will outweigh the initial costs.

It is also important for insurance companies to continuously update their systems and processes to keep up with industry and compliance standards. With advancements in technology, there are constantly new and improved tools to streamline payments processing and enhance security measures. By staying on top of these developments and implementing them into insurance payment operations, insurers can ensure a more efficient and secure payment process for both themselves and their policyholders.

Upgrading systems and adopting new technologies, however, can be a daunting task. It requires time, resources, and a thorough understanding of the current technology landscape. Insurance companies must carefully evaluate their options and choose solutions that best fit their needs and budget.

The initial investment in digital payment solutions, while necessary, can be overshadowed by the complexities of implementation. Upgrading legacy systems and integrating new technologies necessitate a nuanced understanding of existing infrastructure and the constantly evolving security landscape. This is where selecting a vendor with exceptional customer support becomes a strategic advantage.

A robust support network empowers teams to confidently navigate the integration process. Dedicated experts stand ready to address inquiries, troubleshoot technical challenges, and provide guidance throughout each step. This translates to a streamlined implementation, minimizing disruption to core business activities. Prioritize vendors offering comprehensive training resources and ongoing support – a strategic investment that ensures a smooth transition and maximizes the long-term value of your digital payment solution.

.png?width=800&height=233&name=Subheading%20(3).png)

Data Privacy

While built-in tokenization and encryption fortify A2A payments, accelerated payment processing times created by Same Day ACH and instant payments may increase security risks—unless an insurance company has the appropriate controls to mitigate them.

Look for payment processing platforms with enhanced security features, including SOC certifications, and eliminate the need to store sensitive account information. As a Nacha Preferred Partner for ACH technology, Dwolla works with the nonprofit to support sound risk management and security for ACH payments. Nacha develops rules, standards, governance, education, and advocacy while supporting innovation to enhance and enable ACH payments. Through this partnership, Dwolla and Nacha can help ensure fast, safe A2A payment transactions for enterprises.

User Experience

Policyholders’ interactions with insurance companies for payments are often stuck in the past. While the insurance industry itself revolves around risk management and security, the payment process can be a source of frustration for customers.

- Friction and Inconvenience: Forget the days of mailing checks or waiting in line. Today's policyholders expect a smooth and digital experience. Traditional methods create unnecessary friction, hindering timely payments and overall satisfaction.

- Lack of Mobile Optimization: Mobile devices are our constant companions, so insurance payments need to function well in a mobile world. Yet, many insurers haven't adapted to this reality, leaving policyholders juggling clunky interfaces or resorting to outdated methods.

PYMNTS found that convenience, trust, ease of use, seamless user experiences, and faster availability of funds contributed to consumer satisfaction with A2A transactions. A staggering 95% of A2A payment adopters expressed satisfaction with their A2A payment experiences. Additionally, one-fifth of consumers who choose A2A transactions called out the importance of heightened security measures in making their decisions. Increased security is certainly an advantage of pay by bank when compared to the fraud concerns with credit card-based payment methods.

Although pay by bank payments offer a glimpse into a more convenient and secure future, concerns around security remain. The key for insurance companies lies in striking a balance: prioritizing a seamless user experience without compromising robust security measures. By embracing digital solutions and prioritizing a user-centric approach, insurers can transform the payment process into a positive touchpoint for policyholders.

Benefits of Using A2A Payments for Insurance Payments

The insurance industry thrives on stability and security, but traditional payment methods, with their reliance on paper checks and manual processes, can introduce inefficiencies and vulnerabilities. A2A payments offer a digital solution, transforming the way insurers handle finances. Let's explore the key benefits that A2A brings to the table:

Cost Efficiency: A2A payments eliminate the need for intermediaries such as credit card processors (and the fees that come with them), reducing transaction fees significantly. This can be particularly impactful in the insurance industry, where large volumes of transactions are processed regularly. Additionally, these digital transactions eliminate the need for paper checks and the associated manual processes that cost insurers time and money.

Faster Processing: Traditional payment methods, such as paper checks or credit card transactions, can experience delays in processing, require manual steps, and are expensive. Instant transfers, like RTP and FedNow, are almost instantaneous, reducing wait times for insurers and policyholders.

Enhanced Security: Pay by bank solutions are often more secure than other payment methods, as the funds are directly transferred from one bank account to another, eliminating the risk of intercepted or falsified information.

Improved Customer Experience: A2A payments are faster and more efficient than traditional payment methods. This can improve customer satisfaction and loyalty, as policyholders experience a seamless and hassle-free payment process.

Reduced Risk of Fraud: Paper checks can be easily forged or altered, increasing the risk of fraud for insurance companies. Also, credit card payments have a higher rate of fraud than A2A payments. By using A2A payments, insurers can greatly reduce the chances of fraudulent activities and protect their business from financial losses.

Streamlined Payment Processing: Digital payments provide a streamlined reconciliation process for insurance companies. With traditional payment methods, reconciling payments can be time-consuming and error-prone. However, with A2A payments, the entire process can be automated and integrated directly into insurers' financial systems.

Better Cash Flow Management: With faster and more efficient payment processing and increased payment predictability, insurers can better manage their financial resources and make strategic business decisions.

We’ll dive deeper into each of these benefits throughout this guide.

How A2A Payments Can Save an Insurance Company Money

Every dollar saved is a dollar that can be directed toward protecting policyholders. Traditional payment methods, however, can be a major drain on resources, with their reliance on paper checks and manual processes. Enter A2A payments as a game-changer that's revolutionizing how insurance companies handle finances.

Cost Savings with Every Transaction

A2A payments bypass the middleman, eliminating the hefty fees associated with credit card processing. This translates to significant cost savings, especially considering the high volume of transactions insurance companies handle. Plus, say goodbye to the expenses of printing, mailing, and managing paper checks. A2A streamlines operations and keeps your bottom line happy.

Speeding Up the Money Flow

Time is money, and traditional methods can leave insurers and policyholders waiting. Paper checks take days to mail, deposit, and clear, and credit card transactions come with processing delays. A2A payments can be lightning-fast. Especially with RTP and FedNow transfers, funds are transferred near-instantly, improving cash flow and payment predictability for insurers and delivering a more satisfying experience for policyholders.

Building a Fortress Around Your Finances

Security is paramount in the insurance industry, where sensitive data is constantly in play. Data breaches and fraud events can be very costly for a business, and not just financially. Insurers can also experience reputational damage and loss of trust between them and their policyholders. Digital payment solutions offer a layer of protection that traditional methods can't match. Funds move directly between bank accounts, eliminating the risk of intercepted, forged, or altered checks and/or stolen credit card information.

Happy Policyholders, Happy Business

Imagine a world where policyholders can pay premiums or receive claims with just a few clicks. A2A makes this a reality, fostering a seamless and hassle-free process that builds trust and loyalty. Having this competitive advantage can mean increased policyholder acquisition and retention, which leads to increased revenue for the business.

Better Cash Flow Management

No more waiting for checks to clear or manually tracking transactions. With an A2A payments API, you have a clear picture of your cash flow and increased payment predictability, empowering you to make informed business decisions and optimize your financial resources. You also have the information and notifications you need to easily and efficiently track down and solve payment issues, saving your internal teams time and money.

How A2A Payments Improve Efficiency by Streamlining Insurance Payment Processing

In today's digital age, efficiency is king. The insurance industry is no exception, and the burden of manual tasks and outdated payment methods can hinder growth. This is where A2A payments come in, offering a powerful solution to streamline operations and boost the bottom line.

Automation takes center stage. Forget tedious manual tasks and error-prone processes. A2A payments integrate seamlessly with existing systems via APIs, automating everything from data entry to payment processing to payment issue handling. This frees up valuable resources for higher-level tasks while minimizing errors that can disrupt workflows and delay payments. The result? A leaner, more streamlined operation that translates to significant cost savings.

Faster payments, happier policyholders. What if policyholders could effortlessly pay premiums with a few clicks, directly from their bank accounts? Or if insurers could send claim payouts to policyholders nearly instantly, so policyholders get the money they need in the moment they need it the most? A2A technology facilitates this frictionless faster payments experience, leading to improved cash flow for insurers. This win-win scenario not only simplifies the process for policyholders but also provides insurance companies and policyholders with immediate access to funds, enhancing financial predictability and overall operational agility

In a nutshell, A2A payments streamline insurance payment processing, saving time and money, and boosting satisfaction for both insurers and policyholders.

Security Measures in A2A Payments for Insurance Transactions

While integrating A2A payments into your insurance payment system can maximize efficiency and provide a seamless payment experience for policyholders, it’s important to consider security measures and regulatory compliance when implementing A2A payments.

18% of organizations with cybersecurity programs reportedly enhance their ability to drive revenue growth, increase market share and improve customer satisfaction, trust, and productivity. This not only demonstrates the value of cybersecurity for business success but also emphasizes the importance of prioritizing security measures to remain competitive and contribute to overall risk management.

As cybercrime continues to rank among the top 10 global risks of the next decade, businesses across industries must adopt security measures to combat cyber threats and maintain data protection. This is especially necessary in payments and insurance, where businesses are responsible for large amounts of sensitive data.

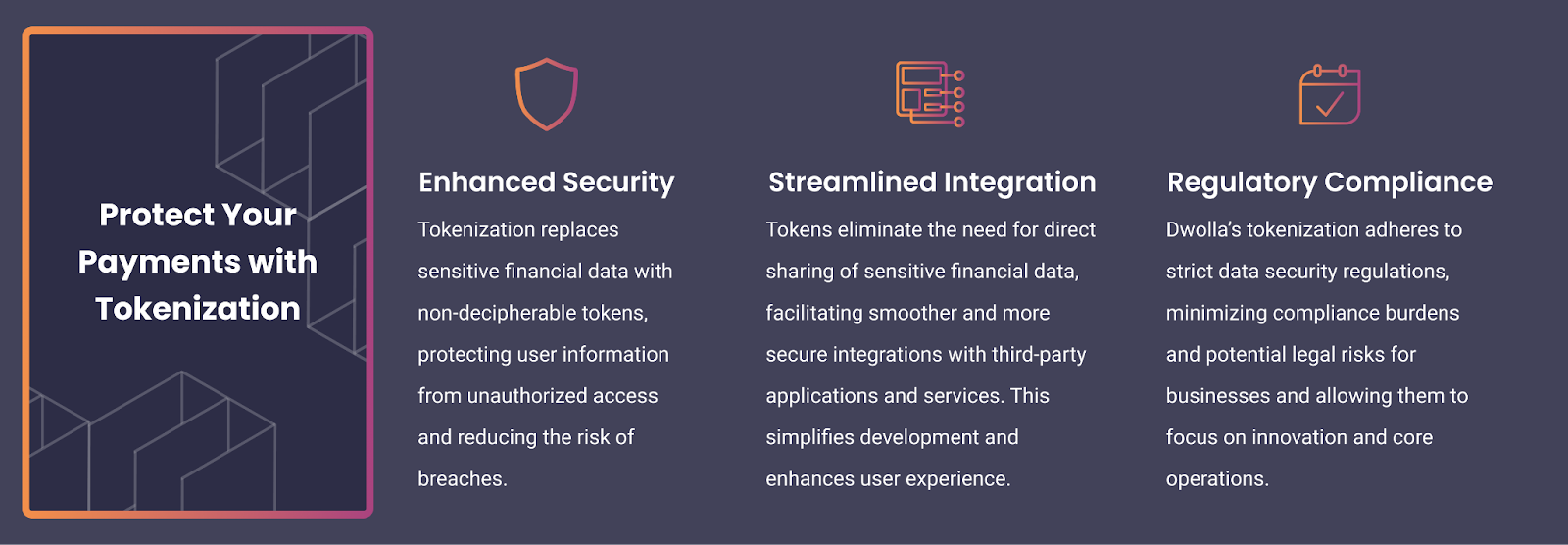

A2A payments can mitigate risks in insurance through encryption, which scrambles the data transmitted between parties, leaving it unreadable for anyone who may intercept it without authorization. Tokenization is another critical element that provides security in A2A payments. By replacing a user’s sensitive data with a unique identifier or token, tokenization eliminates the need to store or transmit private information during the payment process, reducing the risk of data breaches.

The ability to monitor transactions in real time through built-in fraud detection and prevention tools reduces the risk of fraudulent payments and mitigates unauthorized access to sensitive information. Digital IDs and multi-factor authentication provide additional layers of security and are implemented throughout the payment process to verify identity before granting access to accounts or authorizing transactions.

Navigating the technical complexities and ever-evolving security landscape of A2A payments requires a skilled partner. Don't settle for a vendor who simply offers A2A integration. Seek a company that prioritizes both exceptional customer support and robust security measures. Make sure they can demonstrate that they have a tested process for handling security incidents and a business continuity plan that shows they can maintain system uptime as close to 100% as possible.

The vendor you choose should provide a dedicated team of experts readily available to answer your questions, troubleshoot technical hurdles and guide you through every step of the A2A journey. Their support empowers you to focus on core business activities while helping to ensure a smooth and secure implementation.

Your vendor’s commitment to security should be evident in features like encryption, tokenization, and real-time fraud detection. By partnering with a vendor who prioritizes both support and security, you can transform the A2A experience for your business and your policyholders, fostering trust and propelling your insurance company into a secure digital future.

Regulatory Compliance Considerations for A2A Payments in Insurance

In the United States, regulators are working on developing a comprehensive regulatory framework for open banking, a key concept connected to A2A payments. Following the EU’s lead on the Payment Services Directive 2 (PSD2), the Consumer Financial Protection Bureau (CFPB) is establishing industry standards to cover consumer protection, data privacy and security.

Businesses tied to open banking and A2A payments should watch for the latest developments from the CFPB, which proposed the Personal Financial Data Rights rule in October 2023. The goal of this rule is to improve access to financial data and encourage competition across financial products and services. It grants consumers a legal right to share their data and easily switch financial institutions, providing access to this data at no cost to consumers. Additional value is found in enhanced protections to prevent unchecked surveillance and misuse of data, a right to revoke access to consumer data, a departure from risky data collection practices, and fairness across industry standards for both financial institutions and consumers.

As an insurance company utilizing A2A payments, adhering to Nacha rules is also paramount. Regulations established by Nacha ensure secure and reliable electronic fund transfers. Compliance involves following strict data transmission formats, implementing robust authentication measures to prevent fraud, and maintaining accurate and up-to-date recipient information.

Beyond specific regulatory compliance in A2A, industry regulations play a critical role in providing policyholders with secure payment experiences. For example, health insurance companies must comply with the Health Insurance Portability and Accountability Act (HIPAA) to protect policyholder data and maintain trust surrounding sensitive health information. Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations help prevent criminals from laundering money through insurance companies and verify customer identity to prevent fraud, respectively.

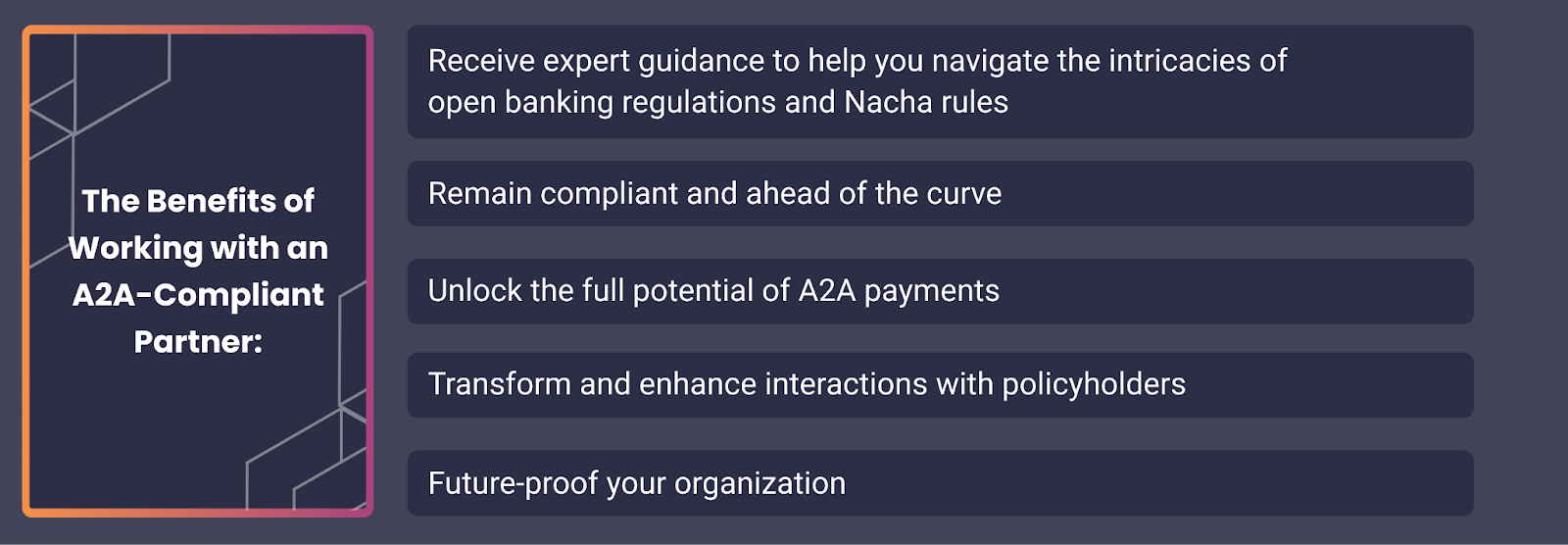

While A2A payments offer a powerful path to modernization, navigating the evolving regulatory landscape can be complex. Selecting a vendor well-versed in A2A compliance is not just a box to check—it's a strategic decision. A knowledgeable partner can guide you through the intricacies of open banking regulations and Nacha rules, ensuring you stay compliant and ahead of the curve.

Remember, fostering trust with policyholders hinges on robust security practices and data privacy. Look for a vendor that prioritizes compliance not just as a checkbox, but as a cornerstone of a secure and successful A2A payment ecosystem. With the right partner by your side, you can unlock the full potential of A2A payments, transforming how you interact with policyholders and propelling your insurance company into the digital future.

Integrating A2A Payments into Your Insurance Payment Operations

Insurers can leverage the power of A2A payments to achieve a complete overhaul of their payment workflows. By integrating pay by bank payment solutions through robust APIs, they can seamlessly connect their existing systems with real-time bank transfers. This eliminates the need for manual data entry and check processing, freeing up valuable resources, and minimizing errors. The result? A streamlined and automated payment process that boosts efficiency and reduces administrative costs.

Integrations between A2A technology and existing systems is the key to unlocking a smoother, faster, and more cost-effective payment experience for insurance companies and their policyholders.

Integrating Dwolla

Leveraging a RESTful API and intuitive SDKs, Dwolla empowers developers to effortlessly integrate secure A2A payments into their insurance applications. They can use the insurer’s current banking relationships, maintain a branded payment experience, and enjoy the benefits of a fast, efficient, flexible, and scalable solution. Whether the insurer is leading a digital transformation, scaling their business, or simply seeking better policyholder interactions, Dwolla has you covered.

Here’s the flow:

- Direct banking connections: Dwolla handles the heavy lifting, working directly with financial institutions to initiate payments on an insurer’s behalf. No need to manage the complexities involved in integrating with banking partners.

- New policyholder sign-up: This process begins when new policyholders sign up for insurance policies and provide their bank account information to authorize and set up automatic payments.

- Automated payment flows: Each month, insurers initiate transfer requests to push/pull funds between their existing commercial bank account and the policyholder’s bank account for monthly premiums or to pay out claims through Dwolla’s API. Once received, Dwolla shares payment instructions for the transfer request with the financial institution that will be the Originating Depository Financial Institution (ODFI) for the transaction. This information allows the financial institution to push or pull funds between the commercial bank account and the policyholder's bank account, crediting or debiting the business’ commercial account for the appropriate transaction amount.

- Real-time updates: The financial institution notifies Dwolla, and Dwolla passes automated webhook notifications back to the insurer, providing them with updates on the payment status.

As a modern solution for the insurance space, Dwolla provides a flexible, secure, and reliable approach for companies navigating policyholder expectations, financial institution partners, and rapidly evolving technology. Through Dwolla’s ease of use and integration, insurers and technology platforms can confidently modernize their payment processes and operations to eliminate legacy systems and improve cash flow and payment predictability.

The use cases below demonstrate how Dwolla’s payment processing platform works for insurance companies.

Digitally Transforming Processes with Electronic ACH Payments

When one pet insurance company spent up to seven days processing reimbursements through manual ACH transfers and paper checks, the search began for a comprehensive payment platform that would reduce processing times and create efficiencies. Dwolla emerged as the solution for this insurance company, saving the company over 92% in costs with automated ACH payments.

By implementing Dwolla, this pet insurance provider reduced the reimbursement processing period, reaching policyholders five days sooner. Electronic ACH payments made this 800% improvement in reimbursement efficiencies possible. Now, this company can rely on Dwolla’s API to provide a fast, versatile, secure and cost-efficient solution.

Embedding ACH API in Insurtech

For another pet insurance company, manual payment processes slowed business operations, impacting growth and policyholder experiences. After embedding Dwolla’s API solution, this insurance provider automated disbursement processes and increased transaction volume by 45% over 12 months.

Dwolla replaced this pet insurance company’s manual process, enabling faster reimbursements via ACH in 1-2 days. Dwolla’s flexible, scalable, and efficient solution enhanced the policyholder experience while saving the insurance provider valuable time and resources.

Future Trends and Innovations in A2A Insurance Payment Processing

As the insurance industry emphasizes digital transformation, increased implementation of A2A payments will naturally follow.

As explained in the Regulatory Compliance Considerations for A2A Payments in Insurance section above, understanding trends and innovations in A2A insurance payment processing depends on a combined broad market outlook and a focus on pay by bank transactions.

Insurtech Market Growth

Digital transformation’s impact on the insurance industry has yielded favorable results for the insurtech market. In fact, the insurtech market was valued at $16.6 billion in 2023 and is projected to grow 41% in eight years to reach $336.5 billion.

Additionally, experts estimate that more than 60% of insurance companies will implement at least one insurtech solution this year. This news aligns with insurtech market stocks, which are among the top performers in 2024. The momentum follows years of downturn in the market as the narrative shifts towards a greater understanding of insurtech.

Embracing AI and ML Technologies

Generative AI and machine learning (ML) will continue to streamline insurance payment processing, improve policyholder experiences and create operational efficiencies. A recent report found that 28% of funding raised in Q1 of 2024 went to AI-centered insurtech companies.

In addition, 60% of insurtech deployments are expected to use AI and ML technologies for risk assessment and underwriting, while more than 70% of insurtech platforms will offer advanced data analytics and predictive modeling capabilities by 2024. This year, around 50% of insurance companies also plan to implement insurtech solutions to enhance customer engagement and digital self-service capabilities.

It will be interesting to watch regulatory compliance updates surrounding AI and ML as these technologies continue to impact so many industries. Insurers should also be aware of policyholder opinions towards AI. When looking at organizational use of personal data, Cisco found that 62% of consumers have expressed concern over AI, with 60% specifically citing a loss in trust due to AI use.

What Do Insurance Market Trends Mean for the Future of A2A Payments?

Digital wallets, paperless payments and contactless transactions are already increasingly popular forms of payment among businesses and individuals, replacing paper checks and invoices. The next phase in payments development will focus on the expansion and widespread adoption of digital tools across industries, aided by open banking and A2A payments.

Cost efficiencies, enhanced security, and convenience are moving the needle, increasing favorable feelings toward A2A payments. Expected to surpass credit cards and other payment processors in popularity, A2A transactions will contribute to an estimated 82% increase in global cashless payment volumes by 2025.

As insurtech companies rebound and grow their market value through digital transformation across all areas of business operations, their focus will be on increasing profitability by solving industry-wide pain points that include managing claims costs, improving underwriting and pricing, and increasing cross-functional teamwork. Leveraging A2A payments helps address these issues so companies can lower costs, create efficiencies and more. As insurtech marketing reaches more people, it can educate them about the speed and security of A2A transactions. This could lead to both insurance companies and policyholders embracing A2A for premium payments and claim payouts.

Insurtech's focus on user experience can translate to seamless A2A integration within insurance processes. Paying premiums or receiving claim payouts will happen effortlessly within the insurance app, making the financial aspects of insurance much smoother for policyholders. Also, insurtech's data-driven approach can unlock new possibilities for A2A payments. By understanding customer needs, insurtech companies could create A2A solutions that cater to specific situations. For instance, A2A payments could be marketed for easily splitting insurance costs with family or roommates. Additionally, the efficiency of A2A could pave the way for innovative insurance models, like on-demand micro-insurance, where real-time transactions are essential.

The future of A2A payments in insurance will also be influenced by the potential of AI and ML (Machine Learning). AI can analyze massive amounts of data to identify fraudulent transactions much faster, saving insurance companies money and protecting customers. Additionally, ML algorithms can streamline claim processing by automating tasks like verifying information and assessing validity. This would lead to quicker claim resolutions and a smoother experience for policyholders.

AI can personalize the insurance experience by using customer data to create individual risk profiles. This could allow insurers to offer tailored coverage options and rates using A2A payment systems that automatically adjust premiums based on real-time risk factors. AI can even improve customer service through chatbots and virtual assistants that answer questions and address issues related to A2A payments. This would provide 24/7 support and free up human representatives for more complex tasks.

The efficiency of AI and ML could also unlock new insurance products, such as on-demand micro-insurance for specific activities, like renting a scooter. AI would assess risk in real-time and facilitate instant A2A payments for the coverage.

With all this potential in mind, insurers also need to keep cybersecurity front of mind. Digital transformation emerges as a solution to curb cyber crimes while implementing the sophisticated technology required to prevent them. In addition to fraud protection and prevention, A2A payments enable real-time visibility into transactions, providing transparency for both policyholders and insurers.

Final Thoughts

A2A payments and open banking are fueling a revolution in the payments industry—one that is expected to expand and reach more industries over the next few years. As adoption grows, the insurance industry will continue to benefit from the ease of use, lower costs, increased speed, efficiency, customization, and security provided by A2A payments.

As a leader in the A2A payments space, Dwolla provides insurers and other enterprises with a comprehensive, modern, and streamlined solution that addresses changing business needs. By implementing with Dwolla, insurance companies can expect optimized efficiencies that result in better use of time and resources, increased savings, improved operations, and enhanced policyholder satisfaction.

Interested in learning more? Schedule a payments consultation today.